You’ve decided to save NZ $5,000 — and then the month passes, the balance barely moved and the goal feels more abstract than it did when you set it. The problem isn’t motivation or income. It’s that saving NZ $5,000 without a rate-based structure is like driving to a destination without knowing the speed you need to maintain. In 2026, the households that reach the NZ $5,000 threshold the fastest share one measurable characteristic: they treat savings rate — the percentage of take-home pay moved to savings before discretionary spending begins — as the primary variable to optimise, not the absolute dollar amount. Everything else follows from that rate.

Here is how the two primary approaches to reaching NZ $5,000 compare across the variables on the casino Spinbit players that determine real-world outcomes:

Savings Rate

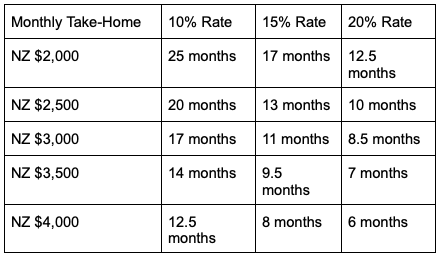

Savings rate — defined as the percentage of monthly net income transferred to a savings account before discretionary spending — is the single variable with the most direct effect on how quickly NZ $5,000 is reached. A 10% rate on a NZ $3,000 monthly take-home produces NZ $300 per month and reaches NZ $5,000 in approximately 17 months. A 20% rate on the same income produces NZ $600 per month and reaches the same target in under 9 months. The difference is not income — it’s the rate applied to the same income.

The projected completion timelines at different savings rates and income levels are:

The minimum monthly surplus needed to reach NZ $5,000 within 12 months is NZ $417. That figure — not a percentage — is the threshold that determines whether the 1-year target is mathematically achievable at your current income. If your monthly surplus after fixed expenses is below NZ $417, reaching 12 months requires either an expense reduction or a rate adjustment, not simply harder effort.

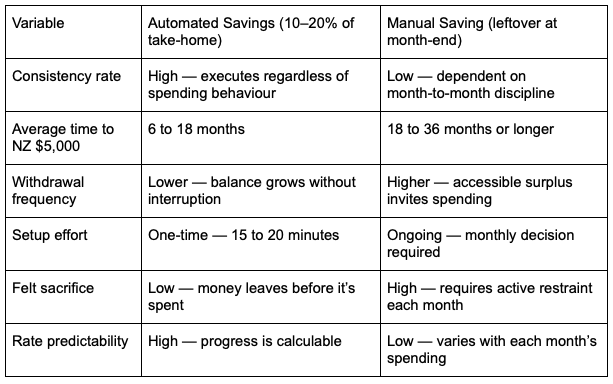

Automation vs Manual Transfers

Automation and manual saving produce measurably different outcomes over a 6 to 18-month period — not because the amounts differ, but because the consistency rate differs. A manual saving decision made at month-end competes with every discretionary spending impulse that occurred during the month. An automated transfer made on payday executes before those impulses have access to the funds. Over 12 months, households using automated transfers reach their savings target at roughly 3 times the rate of those relying on manual month-end deposits, because automation removes the decision from the moment of highest temptation.

At a platform like casino Spinbit, automated session deposit limits produce the same consistency advantage over manually-decided session budgets — the structural mechanism is identical. The decision made in advance, before the session or the spending opportunity begins, consistently outperforms the real-time decision made at the moment. For NZ $5,000 savers, the practical implication is to set the automated transfer rate before the first month begins and not to adjust it downward for at least 90 days, regardless of how the month feels.

The features of an effective automated savings setup are:

- Transfer scheduled for payday or 1 to 2 days after confirmed income arrival

- Destination account held at a separate institution to increase friction on withdrawals

- Transfer amount set at the minimum viable rate first — 10% — and increased only after 60 days of confirmed cash flow stability

- No overdraft protection linked to the savings account — this removes the temptation to treat it as a backup current account

Expense Reduction

Expense reduction, when measured as a percentage of take-home pay rather than an absolute dollar amount, reveals the fastest path to increasing the savings rate without increasing income. A NZ $60 monthly cut on a NZ $3,000 take-home represents 2 percentage points of additional savings rate — enough to move a 10% saver to 12% and reduce the time to NZ $5,000 by approximately 2.5 months. The cuts that produce the largest rate gain per unit of felt sacrifice are consistently found in the same 3 categories: food delivery, overlapping subscriptions and convenience spending on items available at lower cost with 24 hours of planning.

Median discretionary spending data in 2026 shows that households spending above the median in these categories are typically carrying NZ $80 to NZ $150 per month in reducible expense without any meaningful lifestyle change. The categories worth auditing first are:

- Food delivery and takeaway — average monthly spend among regular users: NZ $90 to NZ $160

- Duplicate or unused subscriptions — average number of active subscriptions per household in 2026: 6 to 9, with 2 to 3 used infrequently

- Convenience retail — small-transaction spending that adds up to NZ $40 to NZ $80 monthly without a single purchase exceeding NZ $15

At casino Spinbit, monthly spend tracking tools show players their session-by-session total in clear cumulative form — the same visibility that makes discretionary spending reduction actionable. Seeing NZ $140 spent on food delivery across 14 entries in a month is more motivating than knowing “I spend too much on food.” The number, made visible, is what changes the behaviour.

Withdrawal Frequency

Withdrawal frequency — how often money is removed from the savings account before the NZ $5,000 target is reached — is the variable that most often extends the timeline beyond the projection. A household saving at 15% but withdrawing from the savings account twice a quarter is effectively saving at a much lower net rate, because each withdrawal resets a portion of the compounding progress and reintroduces the psychological cost of starting again.

The 3-month buffer benchmark provides a practical solution. A 3-month buffer — defined as 3 months of fixed essential expenses held separately from the NZ $5,000 savings target — absorbs the unexpected costs that would otherwise trigger savings withdrawals. Without a buffer, the savings account doubles as an emergency fund, which is the structural cause of most withdrawal frequency problems. The 2 accounts serve different functions and should be funded in sequence: buffer first to a minimum of NZ $500 to NZ $1,000, then NZ $5,000 target at full rate. This sequencing reduces withdrawal frequency to near zero for most households because the buffer handles the events that previously interrupted the savings trajectory.

Households that automate at 15% of take-home pay, maintain a 3-month buffer and review their savings rate once per quarter reach the NZ $5,000 threshold in an average of 9 to 11 months — which is the recommended approach for any income tier above NZ $2,500 monthly take-home in 2026.